低碳经济视角下企业环境成本会计核算体系的研究(代写成本会计论文)

摘要

经济的飞速发展使人们的可持续发展意识不断增强,企业环境成本的会计核算体系随之应运而生。我国环境成本会计核算体系在经历过大约二十年左右的发展历程后,在该领域已取得了一定的研究成果,但与欧美发达国家在该领域的研究相比还是有一定的滞后性,同时企业环境成本核算体系本身伴随着与时俱进性随之而来的是不可避免的不健全性和创新性。随着“低碳”这一新兴的理念的提出的是一种更多的寻求排放量的绝对减少的主导思想。本文将企业环境成本会计核算体系的研究同当下热点的低碳经济相结合,在原有的理论和实践的基础上,更进一步提出企业环境成本核算体系在新的形势下的的发展方向。

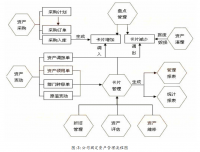

本文所探讨的内容主要是从低碳经济视角下的企业环境成本会计核算体系为出发点和落脚点,其在确认和计量领域,存在要素划分不清晰、计量标准不确定等问题;在归集和分配方面存在成本划分边缘化、核算体系尚不明确等缺陷;在会计信息披露方面存在企业意识有待提高、法律法规不健全等不足。针对文章前部分基于低碳经济视角下的这些问题及原因分析,在文章中的后半部分,又有针对性的对有关具体问题提出了具体建议:在确定和计量领域,加强规范制定标准和加强环境成本的控制;在归集和分配方面,使账户体系和核算方法更加的趋于完整系统;在会计信息披露方面,激发企业的主动性、完善有关的法律法规等。

关键词:低碳经济;企业环境成本;会计核算体系;可持续发展

Studies of Low-carbon Economy Perspective Environmental Cost Accounting System Based On

Abstract

This article will examine the environmental cost accounting system with the current combination of hot carbon economy, in the original theoretical basis and practical problems of further proposed the development direction of the enterprise environment cost accounting system in the new situation of the. Along with the rapid economic development, people's awareness of sustainable development continue to enhance the business environment, along with the cost accounting system came into being. China's environmental cost accounting gone through twenty years of development, we have made some achievements, but the research environment and cost accounting compared to American and European countries there is still a gap, but the business environment along with the cost accounting system itself times of the attendant is not perfect and innovation. With this new concept of "low carbon" there is the pursuit of a more absolute reduction in emissions of thinking. The emerging low-carbon economy study will give new impetus to research and development of environmental accounting

This article focuses on research-based costing system causes of a low-carbon economy Perspective business environment and emerging problems, as well as specific recommendations related environmental cost accounting system Perspective of a low-carbon economy. From emerging low-carbon economy as the starting point of today's enterprise environment cost accounting system analyzes the existing problems, causes and related some feasible recommendations. Environmental cost accounting system based on a low-carbon economy Enterprise Perspective, in recognition and measurement, exist no clear dividing elements, measurement standard uncertainty and other issues; cost divided marginalization and distribution presence in the imputation accounting system is not yet clear and other defects; presence awareness needs to be improved enterprise, inadequate laws and regulations such as lack of accounting information disclosure. Based on these problems and the reasons for the low carbon economy in a view of the front section for the article, in the latter part of the text, respectively, for specific questions put forward specific proposals: the identification and measurement of aspects, strengthening the normative standard-setting and strengthening control environmental costs ; in imputation and distribution, improve and perfect the accounting methods account system; the accounting information disclosure, to stimulate business initiative, improve relevant laws and regulations.

Key words: Low-carbon Economy;Enterprise Environmental Costs;Accounting System;Sustainable Development

目录

一、前言 1

(一)研究背景 1

(二)研究意义 1

二、低碳经济视角下企业环境成本核算体系的问题及原因分析 2

(一)低碳经济视角下的企业环境成本的确认和计量的问题及原因分析 2

(二)低碳经济视角下的企业环境成本的归集和分配的问题及原因分析 3

(三)低碳经济视角下的企业环境成本的会计信息披露的问题及原因分析 4

三、低碳经济视角下企业环境成本核算体系的建议 6

(一)低碳经济视角下的企业环境成本的确认和计量的建议 6

(二)低碳经济视角下的企业环境成本的归集和分配的建议 7

(三)低碳经济视角下的企业环境成本的会计信息披露的建议 8

四、结论 9

参考文献 10

致 谢 12

参考文献

[1]葛家澍,李若山.九十年代西方会计理论的一个新思潮[J].会计研究,1992(5):3-8

[2]范建华.低碳经济的理论内涵及体系构建研究[J].当代经济,2010(4):122-123.

[3]国务院发展研究中心应对气候变化课题组.当前发展低碳经济的重点与政策建议[J].中国发展观察,2009,(08):8-10.

[4]许家林、蔡传里.中国环境会计研究回顾与展望[J].会计研究,2004(4).

[5]蕾切尔·卡逊.寂静的春天[M].长春:吉林人民出版社.1997

[6]强殿英、文桂江.构建企业低碳会计体系的思考[J].会计新视野2010(8),30

[7]国家发展和改革委员会能源研究所课题组.中国 2050 年低碳发展之路:能源需求碳排放情景分析[M],科学出版社,2010(9).

[8]中国会计学会..环境会计专题.中国财政经济出版社2002(8):34-35

[9]李静江.企业环境会计和环境报告书.清华大学出版社2003(7):12-14.

[10]高敏雪.环境统计与环境经济核算.第一版.北京:中国统计出版社.2000:176-202

[11]燕新梅.浅谈企业披露环境会计信息的必要性[J].社科纵横,2005(7).

[12]张以宽.可持续发展战略与环境会计研究[M].中国财政经济出版社,2002.

[13] 蒋先军,吕育立.西方环境会计披露综观及对我国的启示计,2001,(l0):10-13

[14]国家发改委和财政部课题组.“中国碳税税制框架设计”专题报告[R].21世纪经

济.2010,(05).

[15]王立彦.我国企业环境会计实务调查分析.会计研究,1998,(8):21-23

[16]林万祥.成本论.第一版.北京:中国财政经济出版社,2001:32-45

[17] 中国注册会计师协会编.会计[M].北京:中国财政经济出版社.2010

[18]]李玲.关于绿色会计在我国未来发展的两点思考.财会研究,1999(l):17-19

[19]周志方,李晓青.关于国外排污权会计的最新发展进程述评与借鉴[J].经济经纬, 2009(5): 84-87.

[20]张红.论环境会计信息披露[J].科技资讯,2007(9):118-119.

[21]王泽田.上市公司碳管理信息披露框架的国际比较与启示[J].会计之友.2011(9)86-88

[22]周一虹.排污权交易会计要素的确认和计量[J].环境经济,2005,7(3):56-61.

[23]李建发,肖华.我国企业环境报告现状、需求与未来[J].会计研究,2002,(04):58-59.

[24]肖序,陈翔.排污权会计确认与计量的探讨[J].决策与信息,2008,8(9):74-75.

[25]鞠秋云.基于低碳经济视角的企业环境成本核算研究[D].辽宁.东北财经大学工商管理学院,2011:10-60

[26]田志莹,企业环境成本管理与控制之我见[J].会计之友,2007,(05):50-55