建筑施工过程中企业成本控制研究

摘要

建筑行业成本管理的对象是工程项目,为了确保工程项目获利,我们必须做好成本控制。 制定行之有效的成本控制目标, 成本控制的目的是为了合理地降低成本,获取最大的利润。由于施工行业的特殊性,企业在工程项目中标之后对预算进行分解,制定出项目的责任成本和目标利润,企业与项目部应根据工程项目施工地的实际情况,再次对各项施工生产要素(主要指工、料、机)的市场价格进行现场调研,并根据切实可行的施工技术方案和<有关工程施工定额>及有关规定要求,按工程量清单提供的工程数量,重新计算出由项目经理部组织工程项目施工时的市场实际施工总价款.制定这一明细而又具体的成本控制计划,应包括每一个分部分项工程的资源消耗水平,以及每一项技术组织措施的具体内容,它既可指导项目管理人员有效地进行成本控制,又可作为企业对项目成本检查考核的依据.把实际成本控制到目标成本范围内,才能保证企业目标利润的实现。微利时代的建筑施工企业要想在激烈的竞争中求得生存和发展,就必须建立现代企业制度,运用现在的财务管理制度,充分发挥事前预测分析、事中控制、事后分析的职能,严抓企业成本管理和成本控制,挖掘企业潜在的经济能力,以保证企业成本目标的实现,实现企业价值最大化。

关键词:建筑施工企业 成本管理 成本控制

Abstract

The construction industry cost management is targeted at projects in order to ensure project profitability, we need to do a good job cost control. Development of effective cost control, cost control is aimed at a reasonable cost to obtain the maximum profit. As the construction industry's peculiarities, companies bid the project after the budget break down, and work out the responsibility of the project cost and target profit, business and project department should be based on the construction project to the actual situation, once again, the construction of production factors ( mainly refers to workers, material, machine) the market price of on-site research,

Construction in accordance with practical technical programs and "the construction of scale" and related requirements, the bill of quantities provided by the number of projects, re-calculated by the project manager, project organized by the Department during the construction of the actual construction of the total price of the market. The making of this a detail and specific cost-control plan should include some of the items for each sub-project level of resource consumption, as well as a technical organization of each of the specific details, it can guide project managers to effectively control costs, but also as a business-to-project cost of inspections and examinations

Basis. The actual cost of control to the target cost range in order to ensure the business objectives to achieve profit. Low-profit era of construction enterprises in the fierce competition in order to survive and develop, we must establish a modern enterprise system, using the existing financial management system, give full play to advance prediction analysis, a matter of control, hindsight functions, Strict enterprise cost management and cost control, and tap business potential economic capacity to ensure that cost of doing business goals, maximize our enterprise value.

Keywords: Construction Cost Management Cost Control

目 录

摘 要.............................................................2

Abstract...........................................................3

绪论...............................................................4

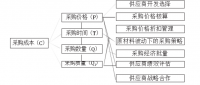

第一章 施工企业成本管理的缺陷分析...................................4

1.1缺乏成本竞争意识,市场应变能力差................................4

1.2成本管理意薄识淡................................................5

1.3成本管理在企业中的地位严重削弱..................................6

1.4成本核算体制不适应市场经济的需要................................6

1.5成本管理方法和手段落后..........................................7

1.6成本管理的内容不全面............................................7

1.7成本管理的方法落后..............................................7

第二章 强化施工企业成本管理的对策...................................8

2.1强化全员成本管理意识,提高全员成本管理素质......................8

2.2 完善成本管理组织和基础工作,建立健全成本管理责任制..............8

2.3丰富和完善成本管理的内容........................................8

2.4以项目管理为重点,推行目标成本管理..............................9

2.5加强宏观管理,改善国有施工企业成本管理的外部环境................10

第三章 对加强施工企业成本管理的几点思考.............................10

3.1解放思想,转变观念..............................................11

3.2要树立效益第一的思想............................................11

3.3加强施工阶段的工程成本控制......................................11

3.4树立科学决策,化解市场风险的责任意识.............................11

3.5对施工过程缺少有效管理,尤其是对材料的管理.....................12

3.6增加索赔的意识.................................................12

3.7牢固树立以人为本的成本管理思想.......................... .......12

总结语.............................................................12

参考文献...........................................................12

致 谢 ............................................................13

绪论

导致我国建筑施工企业利润率的原因可以分为两大部分,一是外部环境,如建筑市场不规范,法律法规好不健全,长期存在向企业论摊派,暗箱操作招投标,业主压价拖欠工程款等,另一个原因是企业内部的原因,现代企业制度的建立只落实在企业名称的改变上,从某某工程处改为某某建筑有限公司,真可谓忽如一夜春风来,千处万处变公司。企业内部机制仍然为老一套,官僚作风严重、管理粗放,不重视人才高成本低效益,浪费和流失吞噬了企业的大部分利润。同时随着建筑业市场的竞争加剧,如何搞好成本控制,使经济效益最大化已经成为施工企业提高自身竞争力的重要途径。但很多施工企业还没有意识到成本控制的重要性,没有将成本控制工作落到实处,或者是成本控制的体系不够完善,致使工程项目施工过程中出现了很多浪费,增加了工程项目的成本。这必将导致施工企业利润的减少,减少企业的内部积累,也会降低施工企业的竞争力,从而阻碍企业的长远发展。中国加入WTO后,国内建筑市场将成为国际市场的一部分,国内建筑企业在应对本国白热化竞争的同时,还要面对国际建筑业集团的竞争压力。国内建筑业早已经进入了微利时代如何加强管理、降低成本、提高效益以成为摆在建筑施工企业面前的紧迫课题。

参考文献

1. 黄东进,施工阶段成本控制探索,科技资讯,2006(31),51。

2. 陈志江,陈静,浅谈项目开发中施工阶段的成本控制,四川建材,2006(2),119。

3. 舒伟,建筑施工企业如何在施工阶段进行成本控制,建筑施工,2002(12)。

4. 尹利福,建筑施工阶段的工程成本即时化控制和管理,科技咨询导报,196-197。

http://www.bysj1.com/ http://www.bysj1.com/html/2968.html http://www.bysj1.com