优化南通一心箱包有限公司成本管理的思考

摘要:本文通过对南通一心箱包有限公司成本管理现状的描述和分析,揭示了中小型箱包制造企业的普遍问题,指

出落后的传统成本管理法下制造费用分配标准单一,造成分配结果不够准确。对本期产品先后采用传统和作业成本

法核算,通过对比得出单位成本差异率,直接表明作业法核算更精准,还有人工、材料等直接影响因素可以通过提

高生产积极性、合理下料来改善。做好成本管理,学习先进管理知识,结合实际总结经验,优化自身管理。只有这

样,才能在保证质量的前提下,尽可能发挥产品的价格优势,打败众多的竞争者赢得市场。

关键词:一心,箱包,成本管理

On the optimization of Nantong Yixin Bags Co.,LTD

Cost Management

Abstract: Through the description and analyze of Nantong Yixin bags CO.,LTD cost management, reveal the small and

medium size bags manufacturing enterprises general problems. The traditional method is falling behind and manufacturing

expenses distribution standard is too simple to get the correct price. By using two different methods accounting and

comparing them, we get the cost difference ratio. We draw the conclusion that manufacturing cost is more accurate under

activity-based costing. There are also some direct factors such as labor and materials, which can be improved by raise

produce enthusiasm and arrange materials rational. Do well in cost management, learn advanced knowledge, generalize

experience through producing and optimize self-management. Only in this way can we play a positive role in terms of price

with quality guaranteed. We will finally win and be the king of the market.

Key words: Yixin; Bags; Costing management

一、引言

任何一个企业,大到跨国公司,小到超市便利店,都离不开成本管理,其中成本

信息尤其重要,社会不断发展,会计人员的职能也在拓展,由简单的记账逐渐向核算

和管理相结合的层次发展。如今,成本管理已经成为企业挤占市场份额的决定性因素,

生产者为了实现追求利润的最终目的,关键性手段就是尽可能降低成本价格,那在保

持相同质量的前提下,要想降低价格,就要重视成本信息和管理,这正是当下制造型

企业所共同面对的问题。

当下,本人在南通一心箱包有限公司从事辅助会计的工作,岗位工作的主要内容

就是协助公司会计人员进行日常记账工作,记录现金、银行存款的流入流出过程和变

化,协助进行存货(原材料、库存商品、周转材料)收入、发出的核算和清查,负责存货日常记账凭证处理,熟悉企业生产流程和成本核算及管理,本文特针对公司成本

管理主题展开研究。

目 录

摘要、关键词 ·····················································································1

一、引言 ···························································································1

二、成本管理概述 ···············································································2

(一)成本管理的含义·······································································2

(二)成本管理的作用·······································································2

(三)成本管理的内容·······································································2

(四)成本管理的方法·······································································2

(五)成本管理的要求·······································································2

三、南通一心箱包有限公司成本管理························································2

(一)南通一心箱包有限公司简介························································2

(二)公司成本管理岗位职责······························································3

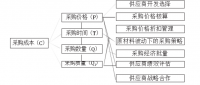

(三)公司成本管理内容····································································3

(四)公司产品及材料情况·································································4

四、公司成本管理现状 ·········································································5

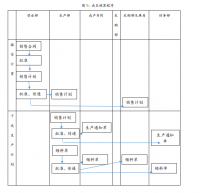

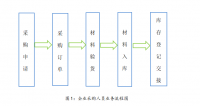

(一)公司成本核算流程····································································5

(二)公司成本核算报表····································································5

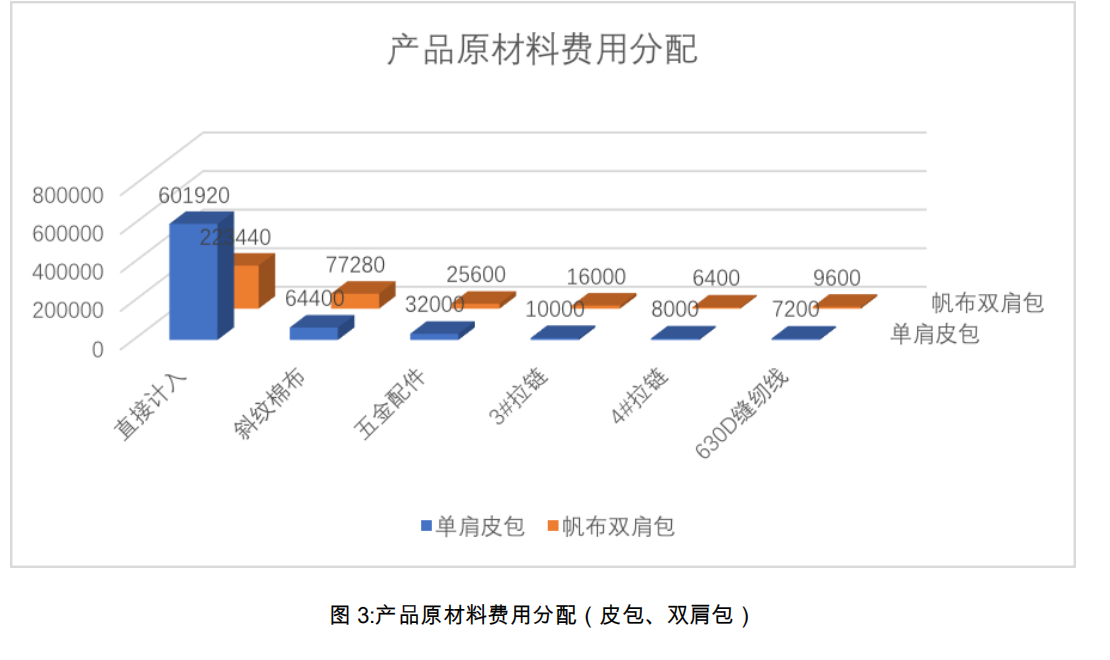

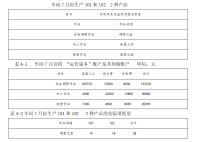

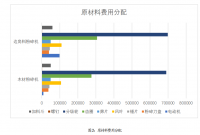

1、产品直接材料耗费情况······························································5

2、产品直接人工制造费用耗费情况················································10

五、公司成本管理现有的问题及分析···················································15

(一)产品成本计算不精确·······························································15

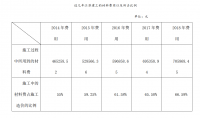

(二)成本费用结构比例变化····························································15

(三)没有考虑非生产性成本····························································15

(四)成本方法简单落后··································································16

(五)员工管理不到位·····································································16

六、优化公司成本管理的建议·······························································16

(一)优化产品成本构成·····································································16

1、关于直接材料 ·······································································16

2、关于直接人工 ·······································································16

3、关于制造费用 ·······································································17

(二)改善制造费用的分配·······························································17

(三)重视期间费用计入成本····························································18

(四)适时更新成本管理模式····························································19

(五)积极评价员工和部门业绩·························································19

七、小结 ·························································································19

参考文献 ·························································································20

参考文献

[1] 周园.我国制造业企业成本核算和管理现状个案调查[J].经济纵横,2013,11.

[2] 朱雅丹.中小企业成本管理困境与出路[J].管理批判,2015,11.

[3] 姜英华.作业成本法在中小企业的应用 [J].财会通讯,2012,9(中).

[4] 安然.中小企业成本管理问题研究[J].商场现代化,2015,26(801).

[5] 冯爽.我国中小企业成本管理问题及对策探析[J].中国市场,2016,42(909).

[6] 谭志坚.企业成本管理存在的问题及对策[J].西部经济管理论坛,2014,7.

[7] 赵丽琼,任畅.作业成本法在精铸企业的应用设计—以 SX 公司为例 [J].管理会计,2016,23.