无锡银科房地产经纪有限公司税务内部控制研究

摘要:随着国家税收政策的改革以及企业管理意识的提高,税务内部控制已经成为企业内部控制的重要内容。近年来,房地产行业的税收制度不断变动,企业要想在激烈的竞争环境中保证自身的持续健康发展,使自身在行业中立于不败之地,就必须在经营过程中时刻关注税收政策的新动向,在实施内部控制时主动实施税务内部控制。本文以无锡银科房地产经纪有限公司作为研究对象,分析其现有的公司税务内部控制情况,并讨论公司内部控制中存在的问题,通过合理化建议的提供,规范其涉税业务流程、降低税收负担和防范税务风险,进而使其能够得以健康持续的发展。(英文摘要做相应修改)

关键词:房地产经纪公司;税务内部控制;内部控制制度

Research on the internal control of Taxation of real estate brokerage Co. Ltd. Wuxi branch bank

Abstract: With the improvement of the state's tax policy reform and enterprise management awareness, the tax internal control has become an important part of internal control. In recent years, the real estate industry continues to change the tax system, the enterprise in order to ensure sustained and healthy development of their own in the competitive environment, make themselves invincible position in the industry, we must always pay attention to the new tax policy in the course of business trends in the implementation of the internal control initiative to implement tax internal controls. Bank Branch Wuxi real estate brokerage company as a real estate agent business competition, facing within the industry, scientific and effective internal controls help to regulate the taxation of its tax-related business processes, reduce the tax burden and to prevent tax risk, and thus enable it to be healthy and sustainable development. This paper is divided into six parts Wuxi Branch Bank real estate brokerage company tax internal controls were studied, the first part of the introduction in the research background and significance, research status and the research content and methods; the second part of the tax-related internal control an overview of the theory on the line; the third part provides an overview of real estate brokers Wuxi Branch Bank Limited; the fourth part analyzed the tax problems of internal control; section V presents the perfect real estate brokers Ltd. Wuxi Branch Bank internal taxation countermeasures control; part VI of the paper to make a conclusion.The Wuxi Yinke real estate brokerage Co., Ltd. as the research object. Analysis the existing corporate tax internal control, and discuss the problems existing in the internal control of the company, through rationalization proposal, specification the tax related business process, so as to reduce the tax burden and anti fan tax risk, and then make it can be sustained and healthy development.

Keywords: real estate brokerage firm,Tax internal control,internal control system

一、引言

(一)研究背景与研究意义

税务内部控制是企业内部控制的重要组成部分,在国家税收政策不断变动的背景下,税务内部控制的重要性也愈加彰显。而随着企业管理层管理意识的提高,其对于税务内部控制的重视程度也越来越高。

作为房地产经纪公司,税务内部控制同样对于公司发展有着不可忽视的重要作用。人们的住房需求不断升高,房产经纪也开始逐步成长为一个产业,在近年得到了迅猛发展,行业之中的竞争也愈加激烈。竞争的加剧对房产经纪公司的管理也提出了更多挑战,如何完善内部管理,提高自身竞争力,在行业中站稳脚跟,是每个房地产经纪公司都面临着的问题。受房价上涨的影响,近年来,国家也连续出台了一些针对房地产行业的相关政策,也在不断对相关的法律法规做出修订。税收环境的改变必然会对房地产相关行业的发展造成影响,公司要想在这样的大环境中获得健康稳定发展,用内部控制完善内部管理是十分重要的,税务内部控制也在这样的大环境中显得尤为重要。

无锡银科房产经纪公司在行业中起步较晚,其税务内部控制方面还十分不成熟,存在一系列问题,在管理上还不完善。公司内部对于税务内部控制的重视程度不够,成效不明显,没有充分发挥税务内部控制的效用。本文以无锡银科房地产经纪公司为研究对象,对其税务内部控制进行研究,最终提出完善其内部控制的相关对策,一方面可以为无锡银科房地产经纪公司税务内部控制的完善提供一定的建议,帮助其通过完善税务内部控制,提高税务管理水平,进而加强其纳税意识,形成更好的公司形象;另一方面,也可以为其他类似的房地产经纪公司提供关于完善税务内部控制的理论基础和参考意见。

目 录

摘要、关键词 1

一、引言 2

1.1研究背景与研究意义 2

1.2国内外研究现状 2

1.2.1国外研究现状 2

1.2.2国内研究现状 3

1.3研究内容和研究方法 4

1.3.1研究内容 4

1.3.2研究方法 4

二、税务内部控制的相关理论概述 4

2.1税务内部控制的含义 4

2.2税务内部控制的原则 5

2.2.1合法性原则 5

2.2.2效益性原则 5

2.2.3针对性原则 5

2.3.4全员参与原则 5

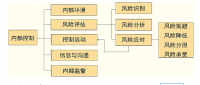

2.3税务内部控制的基本要素 5

2.3.1税务内部控制环境 5

2.3.2税务风险评估 6

2.3.3税务内部控制活动 6

2.3.4税务信息管理与沟通 6

2.3.5税务内部控制的监督和改进 6

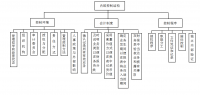

三、无锡银科房产经纪有限公司概况 6

3.1无锡银科房产经纪有限公司基本情况 6

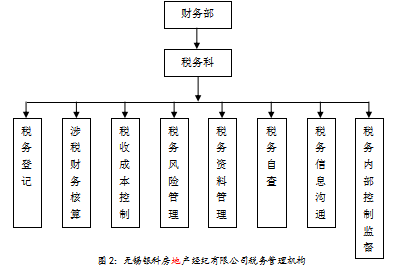

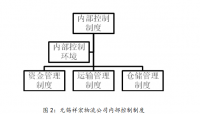

3.2无锡银科房产经纪有限公司组织架构 7

3.3无锡银科房产经纪有限公司涉税业务概况 7

四、无锡银科房产经纪有限公司税务内部控制存在问题 8

4.1税务内部控制环境不完善 8

4.2税务风险的内部控制效果不理想 8

4.3税务内部控制活动不规范 9

4.4税务信息沟通不顺畅 10

4.5税务内部监督不到位 10

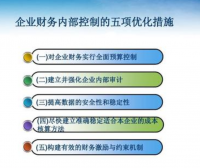

五、完善无锡银科房产经纪有限公司税务内部控制的对策 11

5.1完善税务内部控制环境 11

5.2加强税务风险评估 12

5.3规范税务内部控制活动 12

5.4改善税务内部控制的信息沟通 14

5.5建立健全税务内部监督机制 14

六、总结 14

参考文献 15

参考文献:

[1] Annukka, T.Determinants and consequences of internal control in firms:acontingency theory based analysis[J].Business Management,2009,3(17):43-48

[2] COSO. Internal Control Integrated Framework[R].Executive Summary,1992,9

[3] COSO. Internal Control over Financial Reporting[R].Guidance for Smaller PublicCompanies,2006

[4] 陈爱玲.浅谈加强房地产企业税务管理[J].农村农业农民B,2011(3):32-34

[5] 程亚兰,徐雯靖.加强税务内控建设的思考[J].财政监督,2013(12):45-46

[6] 董燕.企业内部控制实施的必要性探究[J].企业导报,2012(15):89-90

[7] 冯森晓.A 房地产企业税务内部控制问题研究[D].硕士学位论文,湖南大学,2013

[8] 高英.房地产企业税务内控体系的构建探究[J].北方经贸,2012(8):92-93

[9] 国家税务总局.大企业税务风险管理指引(试行)[Z].关于印发《大企业税务风险管理指引(试行)》的通知(国税发[2009]90 号),2009

[10] 黄远.税务内部控制[J].新理财,2008(8):82-83

[11] 李海琴.浅析企业内部控制目标[J].合作经济与科技,2009(6):55-56

[12] 李玉环.内部控制中的信息与沟通[J].会计之友(上旬刊),2014(12):9-10

[13] 刘慧.房地产集团公司税务内控体系的建设与实践.会计师,2014(5):40-41

[14] 刘婕.税务内控创造企业价值[J].经营管理者,2009(12):167

[15] 马海涛.中国税收风险研究报告[M].北京:中央财经大学出版社,2014:39-40

[16] 马谦.谈中小房地产企业税收内控[J].全国商情理论研究,2010(14):57-58

[17] 孙宜.浅析房地产企业涉税风险防范[J].金山,2011(11):85-86

[18] 薛琳.企业内部控制评价指标体系研究[J].商业会计,2011(2):46-48

[19] 亚兰,徐雯靖.加强税务内控建设的思考[J].财政监督,2011(12):45-46

[20] 杨雄胜.内部控制范畴定义探索[J].会计研究,2011(8):46-52